Claims Advocacy in India: How Insurance Brokers Improve Settlement Outcomes

Introduction

The year 2025 saw the Indian insurance policyholders being more aware about their rights than ever before. However, they still find the claims processes difficult to go through. The consumers are frequently feeling disgruntled because of complicated paperwork, waiting for long periods and having disagreements with their coverage, to name a few. In India claims advocacy has evolved as an essential support system with brokers making sure fair treatment and timely settlements for policyholders. The function of brokers has shifted from merely policy placement to a more supervisory role in the safeguarding of policyholder’s rights during claims, which is the most difficult phase of the insurance journey.

The Role of Brokers in Claims Advocacy

Insurance brokers are the middlemen between the people who own the policies and the companies that provide the policies. In the claims setting, their work is not only on the side of the administration. Brokers assist to do the following tasks: they interpret policy terms, they execute the required paperwork, they negotiate with the insurance companies and they even provide legal assistance if there is a conflict. By advocating for policyholders brokers make sure that the insurers honor the coverage promised in contracts with reducing the risk of delays or unfair rejections. By combining the technical aspects of the insurance industry with the role of advocator, brokers have become an important factor for the trust in the system.

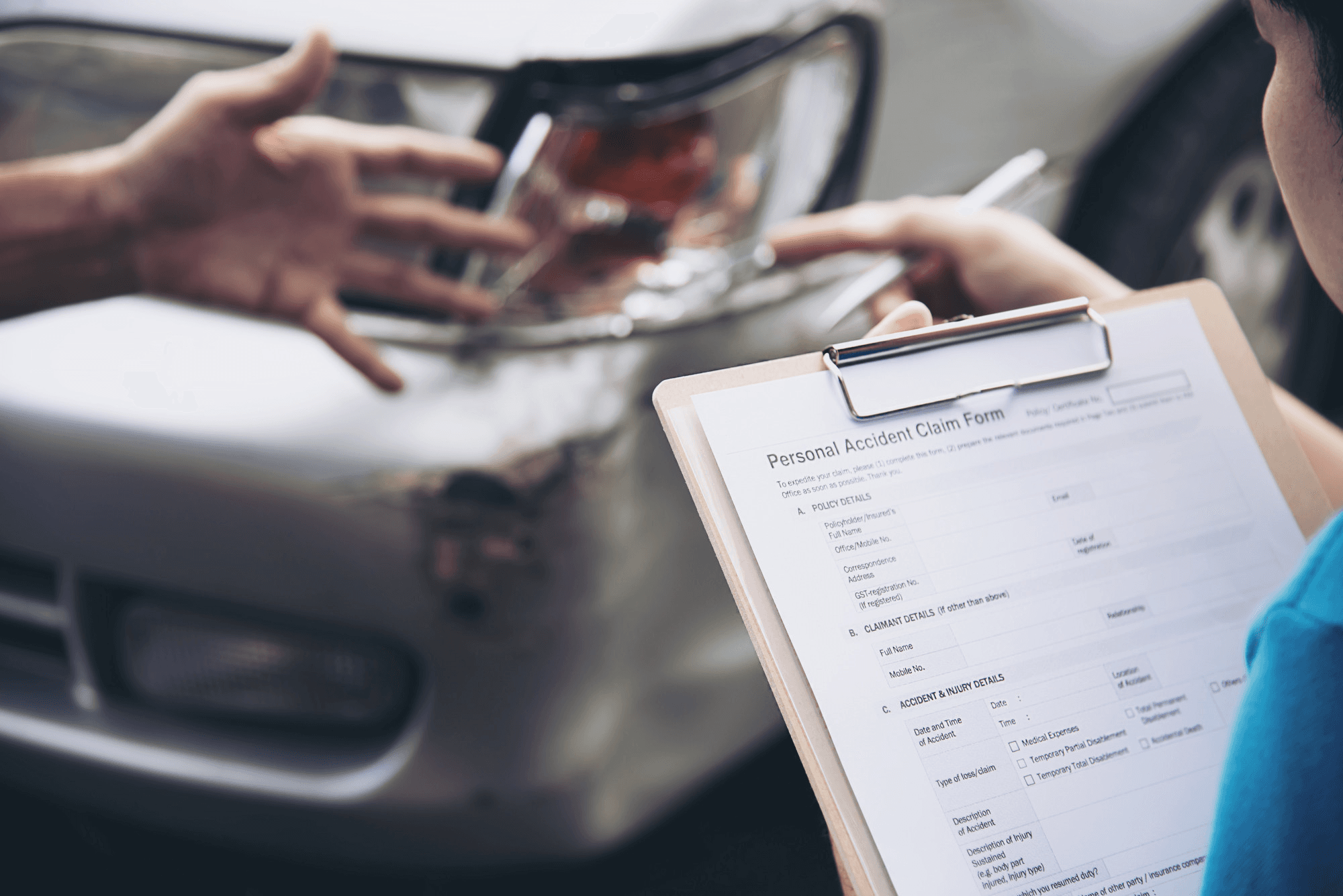

Challenges in Claims SettlementDespite regulatory reforms, claim settlement remains an area of friction in India. The common issues that frequently occur are:

- Ambiguity in Policy Terms: Disputes are usually the result of vague exclusions or unclear definitions of the terms.

- Delays in Processing: Inadequate documentation and procedural inefficiencies are the main reasons that settlements can be delayed.

- Claim Denials: Insurers may refuse claims because the policyholder did not disclose all the facts, informed the insurer late or on technical grounds.

- Under settlement: When claims are only partially paid leaving losses uncovered then the total amount of loss causes dissatisfaction and filing of lawsuits.

These issues have led to a number of court decisions which have emphasized that insurer’s contracts should be interpreted in a manner that is fair and favorable to the insured, especially when the language is unclear.

Legal and Regulatory Framework

In the Indian insurance industry, the Insurance Regulatory and Development Authority of India (IRDAI) is the monitoring body that keeps the insurance companies within certain time limits for their claim settlement and requires them to indicate the reasons explicitly in case of a denial. As licensed intermediaries, brokers have the duty to work in the interest of their clients and to ensure that these requirements are fully complied with. The courts through the Consumer Protection Act have in their judgments always placed the liability on the insurer in such cases where the claim has been rejected in an arbitrary way and without any justification. There are numerous instances where the courts have not only ordered the complete settlement of the claim but also have awarded the complainant money for the inflicted mental agony and the litigation costs. The active participation of brokers diminishes to the lowest amount the possibility of conflicts that become legal by providing the on time execution, accurate documentation and fair negotiation.

Moreover, affected by the introduction of the Digital Personal Data Protection Act, 2023, intermediaries dealing with sensitive claim data must maintain confidentiality on a high level. Violations or data breaches in the claims management process may not only lead to the issuing of fines but also to damage the organization’s reputation.

Benefits of Insurance Claims Advocacy

- Fair Settlements: Brokers represent the rights of the insured and ensure that the claims are not rejections which are false or under settlements.

- Expert Guidance: Brokers assist clients in understanding policy wording thus they can communicate better and the claim application becomes stronger.

- Reduced Legal Risk: With professional support, policyholders are less likely to face prolonged litigation.

- Faster Resolutions: Coordinated communication between brokers and insurers minimises delays in claim settlement.

- Consumer Protection: Brokers’ accountability under law ensures policyholders have an additional layer of support against insurer misconduct.

Brokers as Risk Managers

Beyond claims handling, brokers also assist businesses and individuals in adopting preventive measures to minimise claim disputes. The list can even go to helping a client disclose the true facts of the situation, maintaining the risk management system that helps the company and keeping detailed records. Being proactive will give you the benefits of a smooth claim and that you will comply with the requirements of the policy. Claims advocacy is also a good thing for negotiations with big settlements covering property, liabilities or health where conflict can reach millions of dollars as these are corporate clients. The knowledge of a broker through the documentation process and abiding by the regulatory requirements is what makes the difference between winning and losing cases.

Upcoming of Claims Advocacy in India

As the insurance part enfolds digitisation and the part of brokers in claims advocacy is also developing:

- AI Driven Claims Help: Data tools support brokers identify lost documents and flag discrepancies early which reduces rejections.

- Digital Ledger Records: Established digital records of claims build up transparency and accountability.

- Fusion Models: While digital structure gets better efficiency, brokers can personally guide and it remains important in complicated cases.

Insurance claims advocates in India are going to be in greater demand as the urban risks keep on increasing, climate related claims and regulatory scrutiny. Brokers will keep playing the role of interpreters between the insurers who are bound by contracts and policyholders who have been expecting a fair settlement. They will thus make a key contribution to the achievement of such settlements.

Conclusion

In the constantly changing environment of 2025 it has become crucial that the broker claims support be present for the proper and fair settlement of claims. Insurance brokers take on the roles of champions, mediators and compliance monitors, thereby facilitating rightful payouts to the insured. Claims assistance in India is empowered by justice systems, consumer protection regulations and digital transformation, rekindling the confidence of the public in the insurance sector.