Group Insurance

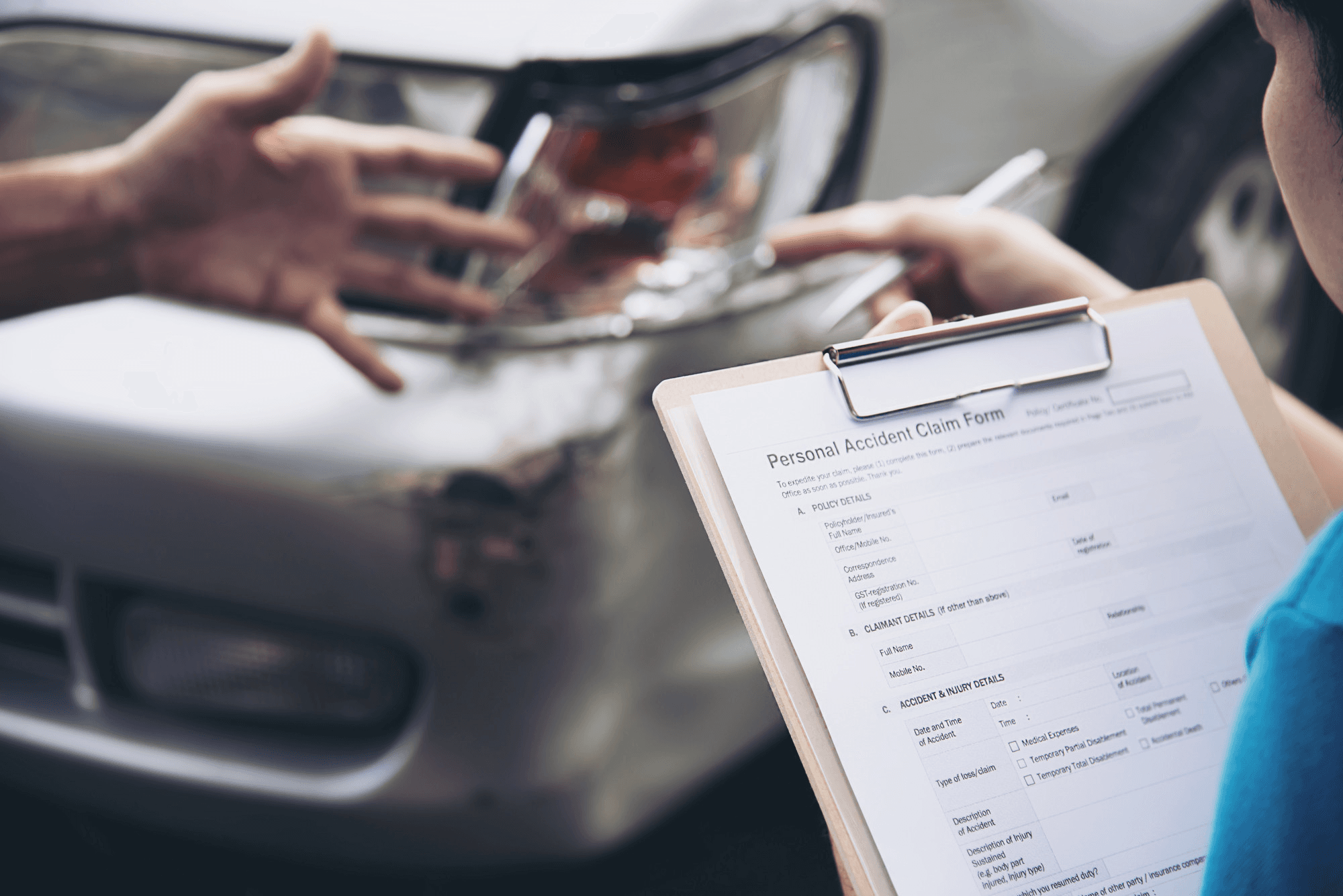

Group InsuranceWhat is Group Personal Accident Insurance?

Learn what group personal accident insurance is, how it works, its key benefits, coverage details, and why it is important for employees and organizations.

Life is very uncertain and mishaps never knock before happening. A sudden accident at work can nearly destroy employees and their families emotionally and financially. In such situations, a group personal accident insurance acts a protective net. A group accident insurance policy is designed for companies or associations so they can provide financial protection to their employees/members. It ensures that if something unexpected happens, employees and their families don't have to face the hard time alone. This offering isn't just about meeting statutory norms; it's a way of showing genuine care and responsibility towards your teams.

There are different types of group accident insurance policies that can be customized according to the needs of different organizations. The flexible nature of these policies makes them useful across sectors.

Best suited for companies and businesses providing coverage to their workforce. Can be tailored to specific industry risk profiles.

Specifically made for employees of an organization. Often extends to contract or field workers as well.

Purchased by schools, colleges, or associations. Protects students and staff against accidental injuries.

Ideal for clubs, trade associations, or professional groups. Provides financial cover to members against accidents.

Group Personal Accident insurance is especially valuable for industries with higher physical risk like manufacturing, logistics, and construction. The coverage is 24/7 and worldwide, meaning employees are covered even outside of work hours. The premiums are very affordable at Rs. 50-150 per employee per month for Rs. 5-10 lakh coverage.

Group personal accident insurance covers death, permanent total or partial disability, and temporary total disability resulting from accidents for all members in the insured group.

Hand-picked reads on group insurance to help you decide with confidence.

Group InsuranceLearn what group personal accident insurance is, how it works, its key benefits, coverage details, and why it is important for employees and organizations.

Group Insurance

Group InsuranceGroup health insurance policies for employees is a main part of employer benefit plans in India. Companies with more than ten employees are required to offer a group medical insurance plan as per the rules established by Insurance Regulatory and Development Authority of India (IRDAI) and Employee’s State Insurance (ESI). This developing change is considered not only compliance but also changing legal requirements and employee expectations. Why Group Health Insurance Is a Legal Essential The social security framework in India is regulated by multiple interconnected laws: The Employee State Insurance Act of 1948 requires coverage for employees in the organised sector with an earning up to INR 21,000 per month. A. The employer contributes 3.25% and the employee contributes 0.75% of the wages. B. Addresses medical care, illness, injury, maternity, disability, family pensions and funeral costs. Insurance Act of 1938 and regulations set forth by the IRDAI A. The IRDAI regulates the terms, pricing and transparency of group insurance as stipulated in Section 34 of the Insurance Act. B. On 1 April 2020, the IRDAI mandated insurers to implement affordable group health plans for organisations returning to operations after the pandemic. Code on Social Security, 2020 Consolidates Employee State Insurance (ESI), Employee’s Provident Fund (EPF), gratuity, maternity benefits and other related benefits into a single framework. Mandatory Coverage: Who & What? Employers with ten or more employees not covered by ESI are required to provide group medical insurance in accordance with the IRDAI circular. Employers subject to ESI are not required to provide supplementary group plans as long as ESI coverage remains in effect. Employees with a monthly income exceeding INR 21,000 who are not covered by ESI but are legally required to obtain group health insurance (GHI) as an alternative. Important Legal Obligations for Employers Obligations of care within common law and statutory frameworks Employers are obligated to ensure workplace health and safety and a responsibility that is both implied in contracts and reinforced by legislation such as the OSH Code 2020. Adherence to the terms set forth by the IRDAI policy The IRDAI mandates disclosures regarding premiums and establishes timelines for claim settlements and even outlines channels for grievance redressal. Insurers are required to provide transparent contracts. Consequences for failure to comply Failure to offer required coverage may attract fines, imprisonment, loss of business licence and reputational harm. Important Differences Between Individual and Group Health Insurance Structure and cost sharing Group policies: employers pay all or part of the premiums; bulk bargaining can lower expenses. Individual: employee paid with modifiable coverage. Scope of coverage Group: includes COVID-19 care, maternity, OPD, ambulance, hospitalisation and pre-existing conditions (often immediate). Individual: may initially rule out pre-existing conditions; requires customised add-ons. Portability Group health plans are subject to IRDAI portability rules which provide continuity in the event of an insurer change. Legal Precedents & Contractual Implications The UK Court of Appeal looked at implied employer duties in insurance benefit plans in Crossley v. Faithful & Gould (2004). Group insurance provisions must be explicitly incorporated into employment contracts in India, with any ambiguities being settled in the worker’s favour in accordance with the rules of contract law. Best Practices for Implementing Group Health Insurance Clarity of eligibility In employment agreements and policy wording which specify covered employees (permanent, contract and trainees). Sufficient levels of sum insured In order to improve retention which is to take into account medical inflation and if possible include parent or family coverage. When appropriate smooth integration with ESI Make sure covered employees are properly identified while avoiding redundant coverage. Audits and policy renewals Engage the finance and human resources and legal departments in yearly reviews of the claims ratio, exclusions and renewals. Communication among employees and the resolution of grievances As required by IRDAI notification has to be sent to staff members of benefits and claim procedures and keep track of grievances. Benefits and Strategic Importance Attracting talent and increasing productivity According to studies insured workers are more dedicated and can take fewer sick days and work longer. Tax advantages Employees benefit from Section 80D deductions for individual health plans and premiums are deductible business expenses. Social and moral accountability Encouraging employee health is in line with Environmental, Social and Governance (ESG) objectives and shows corporate citizenship. Conclusion Employee group insurance is backed by corporate health insurance plans and has transitioned from optional perk to legal imperative in India. The dual framework of ESI Act and IRDAI regulations compels organisations especially those with ten or more employees to implement robust health coverage mechanisms. Employers should view these not as merely statutory burdens but strategic tools to foster wellbeing, loyalty and resilience. Legal perspective: Make policies in accordance with the Code on Social Security 2020 the Insurance Act of 1938 and IRDAI guidelines. Include provisions pertaining to health insurance in employment contracts. To prevent statutory penalties and to keep an eye on compliance. Make use of health benefits to boost output and brand recognition.

Group Insurance

Group InsuranceIntroduction Employee group insurance and corporate health insurance plans have become essential components of employer benefits programs in India, particularly following 2020. Organisations with more than 10 employees are required to offer a group medical insurance plan in accordance with IRDAI and ESI regulations. This transition signifies not only compliance but also the changing landscape of legal obligations and employee anticipations. Why Group Health Insurance Is a Legal Essential The social security framework in India is regulated by multiple interconnected laws: The Employee State Insurance Act of 1948 mandates coverage for employees in the organised sector with earnings up to INR 21,000 per month. A. The employer contributes 3.25% and the employee contributes 0.75% of wages. B. Addresses medical care, illness, injury, maternity, disability, family pensions, and funeral costs. Insurance Act of 1938 and regulations set forth by the IRDAI A. The IRDAI regulates the terms, pricing, and transparency of group insurance as stipulated in Section 34 of the Insurance Act. B. On 1 April 2020, the IRDAI mandated insurers to implement affordable group health plans for organisations returning to operations after the pandemic. Code on Social Security, 2020 Consolidates Employee State Insurance (ESI), Employee’s Provident Fund (EPF), gratuity, maternity benefits, and other related benefits into a single framework. Mandatory Coverage: Who & What? Employers with ten or more employees not covered by ESI are required to provide group medical insurance in accordance with the IRDAI circular. Employers subject to ESI are not required to provide supplementary group plans as long as ESI coverage remains in effect. Employees with a monthly income exceeding INR 21,000, who are not covered by ESI, are legally required to obtain group health insurance (GHI) as an alternative. Core Legal Obligations for Employers Obligations of care within common law and statutory frameworks Employers are obligated to ensure workplace health and safety, a responsibility that is both implied in contracts and reinforced by legislation such as the OSH Code 2020. Adherence to the terms set forth by the IRDAI policy The IRDAI mandates disclosures regarding premiums, establishes timelines for claim settlements, and outlines channels for grievance redressal. Insurers are required to provide transparent contracts. Consequences for failure to comply Failure to offer required coverage may attract fines, imprisonment, loss of business licence, and reputational harm. Important Differences Between Individual and Group Health Insurance Structure and cost sharing Group policies: employers pay all or part of the premiums; bulk bargaining can lower expenses. Individual: employee paid, with modifiable coverage. Scope of coverage Group: includes COVID-19 care, maternity, OPD, ambulance, hospitalisation, and pre-existing conditions (often immediate). Individual: may initially rule out pre-existing conditions; requires customised add-ons. Portability Group health plans are subject to IRDAI portability rules, which provide continuity in the event of an insurer change. Legal Precedents & Contractual Implications The UK Court of Appeal looked at implied employer duties in insurance benefit plans in Crossley v. Faithful & Gould (2004). Group insurance provisions must be explicitly incorporated into employment contracts in India, with any ambiguities being settled in the worker’s favour in accordance with the rules of contract law. Best Practices for Implementing Group Health Insurance Clarity of eligibility In employment agreements and policy wording, specify covered employees (permanent, contract, and trainees). Sufficient levels of sum insured In order to improve retention, take into account medical inflation and, if possible, include parent or family coverage. When appropriate, smooth integration with ESI Make sure covered employees are properly identified while avoiding redundant coverage. Audits and policy renewals Engage the finance, human resources, and legal departments in yearly reviews of the claims ratio, exclusions, and renewals. Communication among employees and the resolution of grievances As required by IRDAI, notify staff members of benefits and claim procedures and keep track of grievances. Benefits and Strategic Importance Attracting talent and increasing productivity According to studies, insured workers are more dedicated, take fewer sick days, and work longer. Tax advantages Employees benefit from Section 80D deductions for individual health plans, and premiums are deductible business expenses. Social and moral accountability Encouraging employee health is in line with Environmental, Social, and Governance (ESG) objectives and shows corporate citizenship. Conclusion Employee group insurance, backed by corporate health insurance plans, has transitioned from optional perk to legal imperative in India. The dual framework of ESI Act and IRDAI regulations compels organisations especially those with ten or more employees to implement robust health coverage mechanisms. Employers should view these not as merely statutory burdens but strategic tools to foster wellbeing, loyalty, and resilience. Legal perspective: Create policies in compliance with the Code on Social Security 2020, the Insurance Act of 1938, and IRDAI guidelines. Include provisions pertaining to health insurance in employment contracts. To prevent statutory penalties, keep an eye on compliance. Make use of health benefits to boost output and brand recognition.

Related guides from our health insurance desk.

Health Insurance

Health InsuranceRunning a startup or small business in Noida's Sector 62 or 63? Group health insurance is no longer just for large companies. Here's what you need to know to cover your team properly.

Personal Accident

Personal AccidentLearn whether personal accident insurance is required in India, who needs it, its benefits, and why it is important for financial protection.

Health Insurance

Health InsuranceIntroduction Life Insurance Corporation of India (LIC) is a household name for life and pension products and many consumers search for “LIC health insurance plans”, “LIC health insurance policy India” or “LIC medical insurance reviews” when shopping for medical cover. Historically LIC has focused on life and savings products rather than standalone health policies, but recent industry and regulatory shifts make this a good time to re-examine what LIC’s role is and what buyers should watch for when comparing health cover. Where LIC stands today (and what’s changing) LIC does not currently dominate the retail health insurance market the way private health insurers do, but it has publicly signalled interest in entering the space by acquiring stakes in a specialist health insurer rather than building a new standalone business from the ground up. This approach would mean LIC-branded health offerings could appear through a joint venture or minority stake in a licensed health insurer, rather than as a direct LIC issued product immediately. At the same time, regulatory action from the Insurance Regulatory and Development Authority of India (IRDAI) and fiscal reforms by the government are reshaping the health-insurance landscape and any LIC foray will be influenced by those rules. Key recent regulatory developments affect waiting periods, coverage of alternative medicine (AYUSH), portability and claim processes; insurers and platforms have been updating product designs to comply. What to expect from an LIC health insurance policy (if/when available) If LIC launches or partners to offer medical cover, you can reasonably expect: Standardised hospitalisation benefits (room rent, ICU, surgeon and diagnostic charges) aligned with IRDAI minimums. Cashless tie ups with a network of hospitals through a third party administrator (TPA) or the insurer’s own network. Optional addons (maternity, outpatient, critical illness riders) offered by most commercial health insurers. These are market norms that any new entrant must follow; product specifics (sum insured slabs, sublimits, copayments) will determine real value. Buying health cover today: practical checklist When comparing policies LIC branded or otherwise focus on the items that determine claim success and long term value: Sum insured and inflation protection choose cover that scales with future medical inflation. Waiting periods for pre-existing diseases check how many years are required before coverage for pre-existing conditions begins. Recent IRDAI guidance aims to reduce unreasonable waiting periods, but individual products still differ. Cashless hospital network and claim turnaround verify the insurer’s network and average claim settlement times. The government is tightening oversight of national claims infrastructure to curb invoice inflation, which should help standardise cashless transactions. Exclusions and sublimits read policy wordings for room rent caps, procedure sublimits and AYUSH coverage. IRDAI’s consumer facing changes are pushing for fewer restrictive sublimits on alternative therapy coverage. Required documents & compliance (quick list) Identity proof (Aadhaar, passport, driver’s licence). Proof of address. Age proof (for eligibility and premium calculation). Medical history / declarations accurate disclosure avoids claim repudiation. These documents and truthful declarations are non negotiable across insurers; portability and renewal benefit from complete records. Recent legal and tax changes that affect premiums A landmark fiscal change in 2025 (implemented by the GST Council and notified by the government) exempted GST on individual life and health insurance premiums effective 22 September 2025. This reduces the effective premium paid by retail policyholders and can make higher cover more affordable. Insurers may, however, adjust commission structures or pricing mechanics as the input tax and accounting impacts are passed through the value chain, so compare final premium quotes. Separately, IRDAI has issued consumer centric guidelines in 2024–2025 aimed at improving transparency, reducing arbitrary waiting periods, ensuring AYUSH coverage without excessive sub-limits and simplifying portability and claims all of which raise the baseline expectations for any insurer offering health plans in India. LIC medical insurance reviews: what reviewers watch Professional reviews of “LIC health insurance” (or any new LIC offering) will typically evaluate: Claim settlement ratio and average claim processing time; Network hospital breadth for cashless service; Pricing vs. comparable private insurers; Policy wordings for exclusions, co-pay and renewability. Because LIC’s brand equity rests on trust and a large customer base, reviewers will pay close attention to how LIC handles post sale service, disclosures and claim disputes. Conclusion If you’re searching for “LIC health insurance plans” or “LIC health insurance policy India”, remember that LIC’s move into health may materialise through a stake in an existing health insurer not necessarily as a direct, standalone LIC policy immediately. Meanwhile, recent regulatory reforms from IRDAI and the GST exemption for retail premiums materially improve affordability and consumer protections across the market. Shop by total cost, wording transparency, network quality and documented claim performance and treat any new LIC health product as you would any other insurer’s offering: read the policy wordings closely and compare final premium and claim terms before you buy.

Broaden your view with a quick read on business insurance.

Business Insurance

Business InsuranceIntroduction Underinsurance in businesses is one of the most common yet overlooked financial risks faced by companies in India. If coverage limits, terms or valuations don’t align with actual risk, a company may have insurance policies in place but still be at risk. To find these gaps, match coverage to operational realities and make sure your policies actually protect you in the event of a claim, it is imperative to conduct a business insurance audit in India. Knowing Underinsurance: It’s Not Just About Low Coverage When the scope of coverage or sum insured is insufficient to cover the actual loss incurred, underinsurance occurs. It usually results from out of date asset valuations, operational changes that aren’t taken into account or a lack of specific coverage for emerging risks in India. It is the insured’s responsibility to declare accurate sums insured and maintain policies up to date; the Insurance Act of 1938 and IRDAI regulations do not automatically prevent underinsurance. In reality, a lot of claims are lowered under the “average clause”, which states that if assets are undervalued, compensation will be lowered proportionately. The Effects of Underinsurance on Indian Businesses Underinsurance can have serious financial repercussions. Due to proportional settlement rules, the insurer may only pay half of the amount if, for instance, your factory’s machinery is worth ₹10 crore but is only insured for ₹5 crore and you sustain a ₹2 crore loss. This strategy has been supported by Indian courts. The average clause was upheld by the court in United India Insurance Co. Ltd. v. Pushpalaya Printers because the insured had assets that were undervalued despite their belief that they were “adequately” insured. Step 1: Conduct a Comprehensive Business Insurance Audit In a business insurance audit in India, all policies of property, liability, cyber, marine, directors and officers (D&O), employee benefits and sector specific coverage are methodically reviewed. Through this process, you can make sure that the policy terms, coverage scopes and sums insured reflect the current state of your business. An audit ought to confirm: Precise asset appraisal (at replacement or reinstatement value) Revised revenue numbers for business interruption insurance Coverage types’ applicability in light of changing risk exposures Step 2: Reassess Asset Valuations Annually Your insurance limits may soon become out of date due to capital investments, inflation and currency fluctuations. Undervaluing assets may be considered misrepresentation since IRDAI requires a fair presentation of risk. Annual valuations help keep your insurance in line with replacement costs, especially for inventory, plant and machinery. Step 3: Review Policy Exclusions and Limitations Underinsurance is caused by both omitted exclusions and inadequate sums insured. Many Indian companies find out too late that their policies do not cover losses from certain risks, such as floods or cyberattacks. Any missing extensions should be found during a policy review, including: Property coverage for earthquakes and cyclones Protection against ransomware and data breaches for online threats Coverage for supply chain interruptions in manufacturing or logistics companies Step 4: Align Coverage with Operational Changes New products, enlarged service areas or new locations all bring new risks as businesses change. These modifications must be reported to the insurer in accordance with the Indian insurance law’s recognition of the principle of utmost good faith. As demonstrated in Satwant Kaur Sandhu v. New India Assurance Co. Ltd., where failure to disclose material facts voids the policy, failure to do so may result in claims being denied. Step 5: Evaluate Business Interruption Coverage Businesses are especially vulnerable to underinsurance when it comes to business interruption (BI) coverage. Since many policies are predicated on antiquated revenue estimates, businesses are left vulnerable during protracted outages. Accurate BI coverage in India ought to show: Present yearly turnover Expected expansion Reasonable turnaround times for operations Step 6: Examine adherence to contractual and statutory insurance requirements Certain industries are mandated to have insurance under the Indian Acts and Laws. For example the Public Liability Insurance Act of 1991 requires specific third party liability coverage for industries that are disastrous, hazardous or catastrophic and the Motor Vehicles Act requires minimum liability coverage for carriers. In order to avoid penalties and ensure that contracts with clients, landlords or lenders are upheld a business insurance audit ensures that all of these legal requirements and compliances are met. Step 7: Track Claims History and Adjust Accordingly Examine whether the terms and coverage limits were adequate if you have had claims within the last 12 months. Trends in claims that are rejected or only partially resolved could point to ongoing underinsurance or misaligned policies. Future disputes are avoided through proactive adjustments. Legal Principles Reinforcing the Need to Avoid Underinsurance When assets are undervalued, Indian courts have consistently upheld insurer’s rights to apply proportional settlement. They also reaffirm the insured’s obligation to accurately and completely disclose risk. Thus, underinsurance can result in disagreements that escalate into expensive litigation in addition to lowering claim payouts. Furthermore, companies still have an obligation to maintain sufficient coverage even though insurers are required by the IRDAI’s Protection of Policyholder’s Interests Regulations to provide clear explanations of policy terms. How to Maintain Adequate Coverage Year Round Avoiding underinsurance is a continuous process. It calls for: Every year, all policies must be audited Revaluations of assets in accordance with market replacement costs When operations change, regular risk assessments are conducted. Speaking with brokers or legal counsel who are knowledgeable about the risks unique to a given industry Businesses can make sure they maintain coverage that actually protects them by instituting these measures. Conclusion In businesses, underinsurance is frequently an undetectable risk until calamity occurs. Businesses can guard against operational failures, legal issues and financial gaps by putting in place a structured business insurance audit India. The most resilient companies view insurance audits as an essential component of strategic risk management rather than as a compliance exercise. In a market that is becoming more unpredictable, this strategy makes sure that coverage changes with the company to safeguard assets, income and reputation.

Commercial Property Insurance

Commercial Property InsuranceIntroduction With India urbanizing so quickly, the commercial property insurance landscape particularly in the commercial sector has undergone a major change. With cities expanding, real estate development is rising and businesses increasingly exposed to natural and man made disasters are driving record demand for commercial property insurance which is reaching unmatched levels. This part of insurance has shifted far behind just asset protection and has become an important part of risk management for enterprises navigating today’s urban challenges. Rising Demand for Business Property Coverage As India’s business centers grow, the chance of damage from fire, floods, earthquakes, theft and cyber attacks increases. The rise in climate related events has made city properties more at risk. Because of this the business property insurance is now needed for all businesses from small stores to big factories. A big change is that there are more businesses that are buying policies that cover not only buildings but also equipment, stock and business interruption. This complete approach shows that companies understand that the business disruptions can cause bigger financial losses than the cost of fixing physical damage. Regulatory Oversight and Policyholder Protection The Insurance Regulatory and Development Authority of India (IRDAI) guides India’s insurance rules. These rules emphasize clear information, fair pricing and quick claim settlements. Policies have to follow strict rules about what they cover to avoid arguments. For cities facing high risks there is an additional cover option such as earthquake or terrorism protection which are commonly advised. Recent court cases show the legal issues that can come up in business insurance disputes. In some cases before consumer commissions and High Courts the insurers had to pay claims because they rejected them using unclear exclusions or not fully explaining the policy. Courts have said many times that insurance contracts must be handled with honesty and that insurers should interpret policies in a way that benefits the policyholders. This legal trend makes it easier for businesses to get compensation and makes insurers more responsible for handling claims quickly and honestly. Urban Risks Driving Policy Growth India’s urban centers face a wide spectrum of risks and insurance adoption is rising accordingly: Natural Disasters like Flooding in metro regions and seismic risks in northern and northeastern states demand specialised coverage. Densely packed industrial and commercial areas have more fire risks so fire riders are important. Because property crimes are up in cities there is a greater need for protection of inventory and buildings. Since businesses rely on being open all the time then even brief shutdowns can lead to big losses which makes business interruption coverage very important. Urban businesses are realizing property insurance is a necessity rather than just an option because of the risks involved. Digital Change in Commercial Property Insurance Commercial property insurance in India has changed because of digital platforms and AI based risk assessment. Tools can now check how strong buildings are and also location based risks even the weather patterns so insurers can set policy prices better. For those with policies the digital claim systems cut down on paperwork and speed up payments. Also devices like fire sensors and security systems are being added to insurance plans. Companies that use these tools to lower risks often get lower premiums which encourages them to take safety steps. Legal Consequences and Responsibilities Business insurance regulations have a few important responsibilities for insurers and policyholders: Insurers: If an insurer mistakenly denies a claim they may face penalties under consumer protection laws. Courts may also order compensation for emotional distress and legal fees on top of requiring the claim to be paid. Policyholders: If a policyholder does not disclose all important information like previous damage or poor safety procedures, their claims may be rejected and they could face legal action. It is critical to be honest and meet all policy demands. Duty of Good Faith: Courts have confirmed that both sides of an insurance deal have to act honestly and if they don’t then they can be sued and lose money. Strategic Considerations for Businesses Businesses in cities should do risk assessments that look at both building risks and location related risks when picking insurance. Think about using extra coverage options: Things like coverage for natural disasters, theft and business problems can add important protection in cities. Follow the law and be honest when you apply and follow safety rules you can avoid problems with claims and get better insurance options. Use of technology: Prevent problems like fire systems as they have security cameras and they keep monitoring tech which can lower risks and also even lower your insurance costs. Keep up with legal news: Knowing about court decisions can help you be ready for possible legal arguments. Conclusion Commercial property insurance in India has evolved because of the digital platforms and AI based risk assessment. By 2025 the business property insurance will be an important part of how companies in India deal with the risks of fast-growing cities. The higher need for this kind of insurance shows that risks are increasing and that people know more about how insurance can protect them financially. Because rule makers want things to be clear, courts are protecting the rights of people with insurance and technology is making coverage smarter. Property insurance is becoming a main part of keeping businesses going. For businesses it’s vital to pick complete policies, follow the rules and take steps to prevent problems in cities.

Business Insurance

Business InsuranceIntroduction Mergers & Acquisitions Insurance in India also known as transactional risk insurance has evolved as an important tool for deal makers to evaluate and decrease risk in complicated M&A transactions. What is M&A Insurance(Transaction Risk Insurance) M&A insurance (Transaction risk insurance) refers to the policies that protect parties in a merger or acquisition from losses arising from certain transaction risks. These include breaches of representations & warranties (R&W), undisclosed liabilities (e.g. tax liabilities), environmental or regulatory risks or other post closing liabilities. Parties use insurance to shift certain risks to insurers, reducing exposure, improving certainty and often facilitating effortless deal closure which is way better than only relying on contractual indemnities. More Usage of M&A Insurance in India Speed and planning: Caps and escrow can be simplified because insurance can replace or support seller indemnities and claim negotiations. More competitive insurance market: Premiums are now more competitive. Insurers provide broader coverage which makes it possible for smaller deals with lower enterprise value to get insured. M&A Insurance: Legal & Regulatory Structure Insurance Regulatory & Development Authority of India (IRDAI): The regulator for insurance business. Any transactional risk insurance policy will be under its supervision. Insurance Act 1938 and IRDAI Act 1999: The Insurance Act manages insurance contracts. The IRDAI Act controls regulation of insurers including registration, solvency, conduct of business, disclosures, etc. Proposed Insurance Laws (Amendment) Bill 2024: In 2024, the Indian government has proposed extensive amendments to the Insurance Act and IRDAI Act. These may influence rules for registration, operational matters and risk allocation regulations. Parties using M&A insurance should look out for these developments. Company Law, Securities Law & FDI Regulations: M&A usually involves regulated sectors, foreign investment, securities rules (example for listed companies), disclosure obligations and antitrust/competition law (example CCI approval). This establishes what risks are insurable, what exposures must be disclosed and the drafting of R&W. Recent Changes & Compliance Trends India’s regulatory and legal environment has seen changes that affect how transaction risk insurance is used, structured and enforced: Use of ‘buy side’ policies is more common: In general, the seller side has warranty/indemnity risk. Increasingly, buyers are getting insurance to cover their post closing claims if the seller fails to perform. Following international rules: Indian companies and insurers are changing policy wordings, jurisdiction rules and coverage to reflect global standards as international transactions are rapidly rising. Law firms and brokers also play an important part in customising these policies. Litigation and regulator: Regulators like IRDAI, tax, environmental and data protection authorities are paying closer attention. Hidden or undisclosed liabilities like tax or environmental issues have caused recent claims and this makes compliance and full disclosure very important. M&A Insurance Policies Structure Parties should consider these following points to manage transaction risks effectively using M&A insurance: Scope of coverage: What representations & warranties are insured, which liabilities are excluded (example known risks, fraud or certain regulatory risks). Negotiating timelines for disclosure. Retention/deductible: How much amount of risk remains with the seller or buyer affects premium and enforceability. Policy limits & claims period: How long after closing can claims be made (it’s usually between 2 to 4 years) or What is the maximum amount of money that can be lost. Tail or run off coverage: After the deal for the seller side, there could be liabilities that can come up later and buyers may require sellers to maintain certain insurance or give indemnity for a period or insurance companies might offer tail coverage. Change in control clauses: Many policies include clauses that modify coverage if the corporate structure changes significantly (postmerger) or after acquisition to prevent coverage gaps. Disclosure and due diligence: The quality of due diligence directly influences risk perception. Misstatements or omissions can result in claim denials. Comprehensive information exposure helps minimise insurer objections. Recent or Emerging Legal Risks & Must Knows Tax liability & DTAA clauses: With international transactions, tax treaties (Double Taxation Avoidance Agreements) and local Indian tax regulations pose potential undetected liabilities. Insurers may require enhanced disclosure. Data Privacy / Cybersecurity Laws: Upcoming laws in India (like Data Protection Bill, etc.) maximise liability exposure for companies and insurers are increasingly enquiring about compliance with such laws. Failure in this area may result in uncovered losses. Benefits vs Challenges Benefits: Decreases post closing risk for buyer and seller. Facilitates in faster closings when contractual risk problems are insured. Increases credibility with external investors or lenders. Challenges: Cost of premiums (particularly for complicated or high risk sectors). Time and negotiation required to agree on policy wording, procedure of disclosures. Insurers may deny covers for specific known but not fully disclosed risks. Possible overlap, dispute or conflict with other insurance, indemnities or warranties. Conclusion M&A insurance (transactional risk insurance) has become a foundation of India’s transaction framework. Buyers and sellers negotiate with greater confidence, shorten timelines and unlock transactions by transferring critical risks to insurers which otherwise might delay or obstruct operations. To increase its value, dealmakers have to stay alert for regulations developments, structure policies carefully and coordinate insurance coverage with industry regulations.