Personal Accident

Personal AccidentIs Group Personal Accident Insurance Worth It for Employees in India?

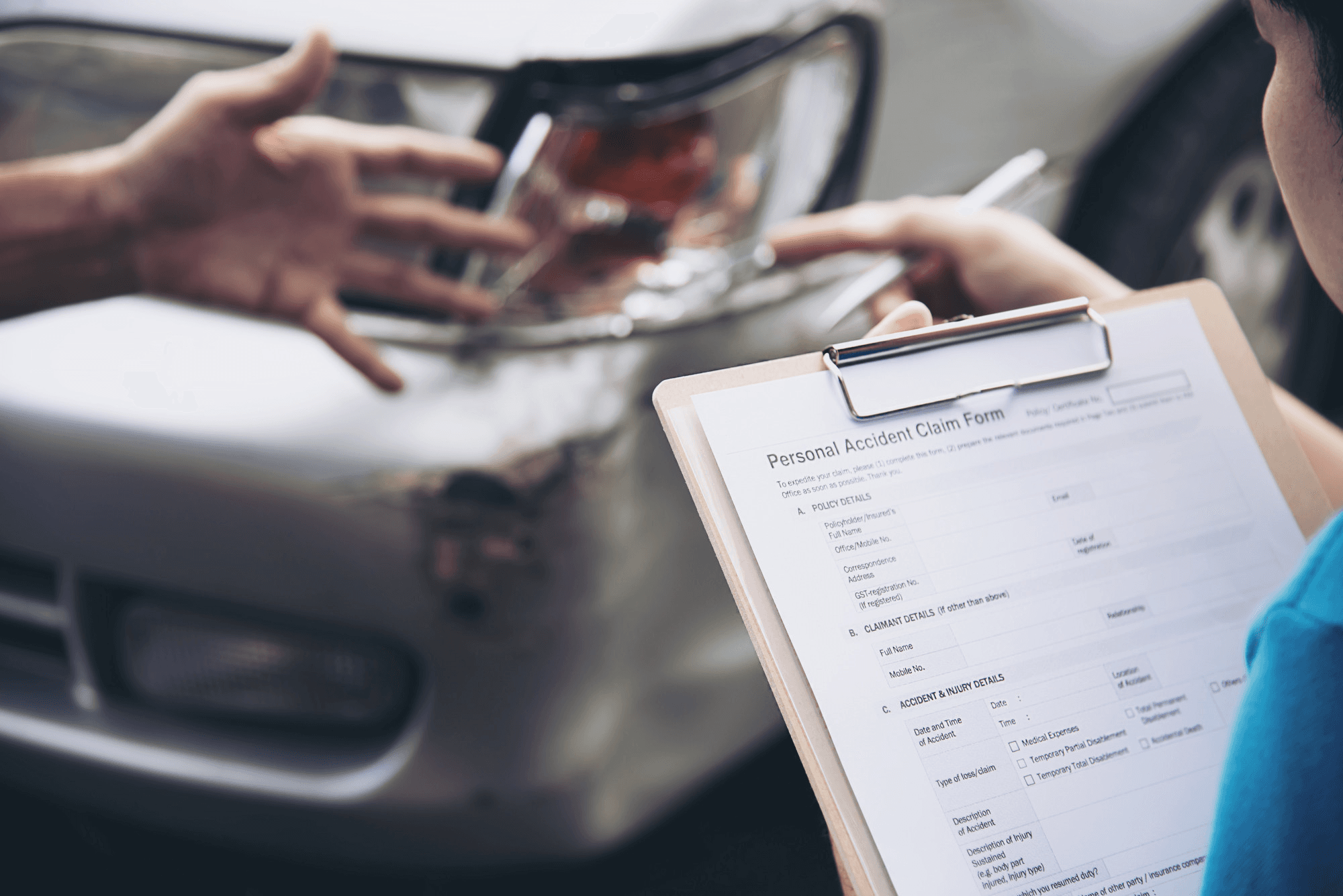

Introduction Group personal accident insurance India has become increasingly essential for employers wanting to protect their workforce against unforeseen incidents as there is a high chance of evolving risks and on site injuries where insurance has gained attention as a helpful inclusion in employee benefit packages across organizations of all sizes. Group Personal Accident Insurance Group personal accident insurance (GPAI) is a policy that covers employees altogether against accidental death, permanent disablement and temporary disablement (in many cases). Customised for a group like company staff or association members where this insurance offers financial protection when there is an unpredictable accident. In India where workplace and travel related incidents are common, GPAI provides crucial coverage to lower economic fallout. Significance of Group Coverage for Employers Cost Effective Premiums: Group schemes influence economies of scale which is better than individual accident plans. Insurers usually offer lower per person premiums under group arrangements which makes it inexpensive for employers while increasing employee security. Simplified Administration: Holding on to a single insurance policy instead of numerous individual ones simplifies HR operations. PolicyWings clients can appreciate how group personal accident insurance decreases paperwork, eases onboarding and makes claims processing quick because of systemised coordination. Moral and Competitive Corner: In a competitive job market offering accident insurance shows that an employer values employee well being. This not only increases morale but also enforces retention and attracts talent by differentiating compensation packages. Benefits of Group Coverage for Employees Financial Security after an Accident: If an unfortunate accident results in permanent disability or death then the lump sum compensation eases financial load on families. Access to Interim Income Support: Some policies include temporary total or partial disablement cover which provides income in case of an employee being incapacitated for a period. This type of benefit maintains employees and their families during recovery. Quick Claim Processes: Group policies usually have standardized claim mechanisms which are managed at the employer level which allows employees to file claims easily without navigating complicated individual procedures. What Employers Should Consider When Selecting a Plan Extent of Coverage: Group personal accident insurance has different offers. Employers must check if the policy includes death, permanent and temporary disability and sometimes, medical expenses or daily hospital cash. Wider coverage has prices slightly higher but provides comprehensive protection. Coverage Limits must be Adequate: having adequate coverage limits per employee is essential. Compensation should be relevant to local cost of living, typical wage levels and potential liabilities from accidents. Not insuring rightly could leave families inadequately supported. Inclusions and Exclusions: Policies often exclude risky activities (for example extreme sports or non work related accidents). Employers have to review the list carefully to make sure that the coverage matches employee real world risks particularly in industries like logistics, manufacturing or field services. Record of Claim Settlement: Evaluating the insurer’s reputation for claim processing in India is essential as well. A quick transparent claim experience increases employee trust in the benefit and it also reinforces its value. Add On Features: Optional riders like repatriation of remains, ambulance charges, funeral expenses or education benefits for dependents can enhance policy utility a lot. It’s optional but benefits are usually appreciated by employees. Clarifying Common Concerns One common doubt is whether GPAI overlaps with other employee insurance coverage. In India, many companies provide group health and life insurance and still those policies may not fully cover accidental disability or death arising from nonhealth related causes. Accident specific coverage adds an additional layer of protection customised for sudden and unintended events. Another doubt is whether smaller organizations can afford group personal accident insurance. Yes, they can. Many insurers provide entry level group plans that limit the amount of costs while providing essential protection and they are flexible as well. As the workforce evolves the coverage tiers can balance accordingly. Improving Your HR Benefits Package Converting group personal accident insurance into overall employee well being frameworks strengthens employer branding. When put together with group health, life and wellness offerings then GPAI is a complete trio of risk protection. This strengthens policies marketed under “employee benefit insurance”, “corporate accident policy”, or “accident insurance for employees India”. And proactively communicating these benefits during orientation and periodic HR outreach helps employees understand them which improves perceived compensation value. Advice for Maximizing ROI on GPAI Conduct a risk assessment to adjust coverage to your workplace profile Survey employee concerns around security and financial uncertainty Compare insurer quotes focusing on claim settlement ratios and coverage scope Educate employees on policy particulars especially the claims process Review policy annually to customise benefits or coverage limits as needed Conclusion Group personal accident insurance India offers a cost efficient, morale boosting and administratively effective way to add adequate protection for employees. In circumstances where accidents can ruin lives and livelihoods, this coverage plays a critical role. For employers it’s not just an expense but it’s an investment in workforce resilience and employer brand differentiation.