Family Floater Health Insurance Plan: Tips & Benefits

Family Floater Health Insurance Plan: Tips & Benefits

Table of Contents

- Family Floater Health Insurance Plan: Tips & Benefits

- What is a Family Floater Health Insurance Plan?

- Why Is Family Floater Insurance Better Than Individual Health Insurance?

- Perks of Having Family Floater Health Insurance

- Tips to Choose the Right Family Floater Health Insurance Plan

- To Conclude,

- Some Frequently Asked Questions

Family Floater Health Insurance Plan: Tips & Benefits

It goes without saying that having health insurance in the modern era is like having an umbrella protecting you from the downpour of medical bills.

But having a family floater health insurance policy shields you and your loved ones from the strong winds and rain of medical bills, much like a covered roof.

With the rising cost of insurance plans in our country, it just burdens our pockets to get health insurance for all our family members individually.

That is why, there is a family floater health insurance that covers our entire family without putting holes in our pockets.

Let’s understand everything in detail about a “family health insurance plan” and how it’s better than an individual health insurance plan.

What is a Family Floater Health Insurance Plan?

Family floater health insurance is also termed a family health insurance plan.

And it’s very evident from the name itself, that a family floater plan gives medical coverage to the entire family.

In family health insurance, a single sum insured is shared among all members. So, any member of the family can avail the insurance up to the policy’s limit.

So, with a single-family health insurance plan, the primary policyholder can insure multiple family members under a common sum.

You are basically paying a single premium to insure yourself, your spouse, children, and parents (based on the type of plan).

Why Is Family Floater Insurance Better Than Individual Health Insurance?

To determine which medical insurance plan is better for your family, it is essential to compare family floater health insurance with individual health insurance.

So, let’s understand this with an example.

There are two friends, Mr. Singh and Mr. Yadav. They both are a family of four. However, Mr. Singh took family floater health insurance, and Mr. Yadav took an individual health insurance plan for his family.

Now, Mr. Singh holds a floater health insurance policy worth Rs. 8 lakh. So, here, the total amount of health coverage is Rs. 8 lac for 4 members.

Whereas, Mr. Yadav, with an individual health insurance plan, has a policy amount of Rs. 2 lakhs (for each member). So, the total amount of health coverage in his case is also Rs. 8 lac.

Both families faced medical emergencies at the same time, and the hospitalization and treatment expenses incurred by both families were Rs. 5 lac.

In this case, Mr. Yadav only got Rs. 2 lac after his claim was reimbursed; he was still required to pay the remaining Rs. 3 lac out of pocket.

However, in Mr. Singh’s case, the maximum policy amount was Rs. 8 lac, so he was reimbursed for Rs. 5 lac.

As a result, Mr. Singh is happy because he did not have to pay for any of the hospitalization expenses out of pocket.

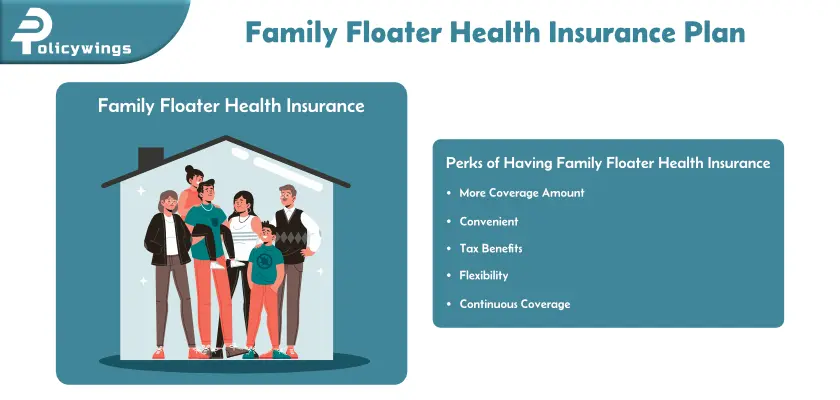

Perks of Having Family Floater Health Insurance

Some of the major benefits of having a family floater plan are:

- More Coverage Amount

In family floater insurance, each family member has access to a total sum insured. So a single plan with a shared sum insured is generally cheaper than buying individual policies. - Convenient

Managing one policy for an entire family is much more convenient than handling multiple policies. - Tax Benefits

Similar to other health plans, a family floater plan also lets you avail of tax deductions on the paid insurance premium. The premium paid for a family floater plan is eligible for tax deduction under section 80D of the Income Tax Act, India. - Flexibility

A family floater plan provides flexibility by allowing you to add or remove family members whenever needed, making the insurance plan adaptable to changing family situations. - Continuous Coverage

Generally, health insurance expires on the death of the insured. However, a family health insurance plan continues to offer coverage to the family even after the demise of a particular family member.

Tips to Choose the Right Family Floater Health Insurance Plan

Before you buy a family floater plan, it’s important to know what points to consider to get the best floater health insurance plan.

Some of the factors, that you should consider while buying a family health insurance plan are:

- Family size and age

First, decide the number of family members you need to cover and their age groups. Because younger individuals might need lower coverage as compared to older individuals - Total sum insured

Remember to choose a sum insured that covers all your potential medical expenses. For this, you can take into account some factors like rising healthcare costs and the family’s medical history. - Plan Coverage

Choose a plan that offers all-around coverage for all the hospitalization expenses, pre and post-hospitalization costs, and ambulance services. - Network Hospitals

Check if the plan offers a wide network of hospitals for cashless hospitalization facilities. - Exclusions

Review the policy wordings carefully to understand any exclusion like pre-existing conditions or specific treatment. - Renewability

Go for a family insurance plan that guarantees renewability so that you can get continuous coverage throughout your life. - Claim settlement ratio

Also, research the insurance company’s claim settlement ratio to understand their efficiency and compatibility in settling and handling claims.

To Conclude,

A family floater health insurance plan is a valuable protection tool that you can gift to your family.

However, properly understand how these plans work and consider your family’s needs before choosing the right and affordable health insurance plan.

You can also compare rates, but if you are short on time, just call our advisors and they will walk you through all the important points for a family floater health insurance plan.

Some Frequently Asked Questions

What is a family floater health insurance?

A family floater plan is made to cover several family members’ medical expenses under a single insured amount. Any family member can then use the insured amount to pay for their medical bills.

Which is better family floater or individual insurance policy?

Both are good health insurance plans thus, the better can only be decided based on your situation. For instance, if you have a family that depends on you for its well-being than you should choose a family floater plan. But, if you wish to get yourself insured, than go for an individual health insurance plan.

What are the advantages of a family floater health insurance policy?

The list of benefits that you can get by buying the aforementioned insurance plan are:

- Pre-hospitalization cover

- Ambulance cover

- In-patient hospitalization coverage

- Post-hospitalization cover

- And lifelong renewability

Who Cannot be covered under a family floater policy?

The individuals like nonfamily members, siblings, relatives, and those with pre-existing medical conditions can not be included in a family floater policy. Also, there are some age restrictions regarding the children and elderly family members are applied to a family floater plan.

What is family floater travel insurance?

A family floater travel insurance policy, like a family floater policy, is intended to protect a family traveling together against a variety of risks, such as medical emergencies, trip cancellation, misplaced luggage, and more.

{"@context":"https:\/\/schema.org","@type":"FAQPage","mainEntity":[{"@type":"Question","name":"What is a family floater health insurance?","acceptedAnswer":{"@type":"Answer","text":"

A family floater plan is made to cover several family members’ medical expenses under a single insured amount. Any family member can then use the insured amount to pay for their medical bills.<\/p>"}},{"@type":"Question","name":"Which is better family floater or individual insurance policy?","acceptedAnswer":{"@type":"Answer","text":"

Both are good health insurance plans thus, the better can only be decided based on your situation. For instance, if you have a family that depends on you for its well-being than you should choose a family floater plan. But, if you wish to get yourself insured, than go for an individual health insurance plan. <\/p>"}},{"@type":"Question","name":"What are the advantages of a family floater health insurance policy?","acceptedAnswer":{"@type":"Answer","text":"

The list of benefits that you can get by buying the aforementioned insurance plan are:<\/p>

- <li aria-level=\"1\">Pre-hospitalization cover<\/li><li aria-level=\"1\">Ambulance cover<\/li><li aria-level=\"1\">In-patient hospitalization coverage<\/li><li aria-level=\"1\">Post-hospitalization cover<\/li><li aria-level=\"1\">And lifelong renewability<\/li><\/ul>"}},{"@type":"Question","name":"Who Cannot be covered under a family floater policy?","acceptedAnswer":{"@type":"Answer","text":"

The individuals like nonfamily members, siblings, relatives, and those with pre-existing medical conditions can not be included in a family floater policy. Also, there are some age restrictions regarding the children and elderly family members are applied to a family floater plan. <\/p>"}},{"@type":"Question","name":"What is family floater travel insurance?","acceptedAnswer":{"@type":"Answer","text":"

A family floater travel insurance policy, like a family floater\u00a0 policy, is intended to protect a family traveling together against a variety of risks, such as medical emergencies, trip cancellation, misplaced luggage, and more.<\/p>"}}]}