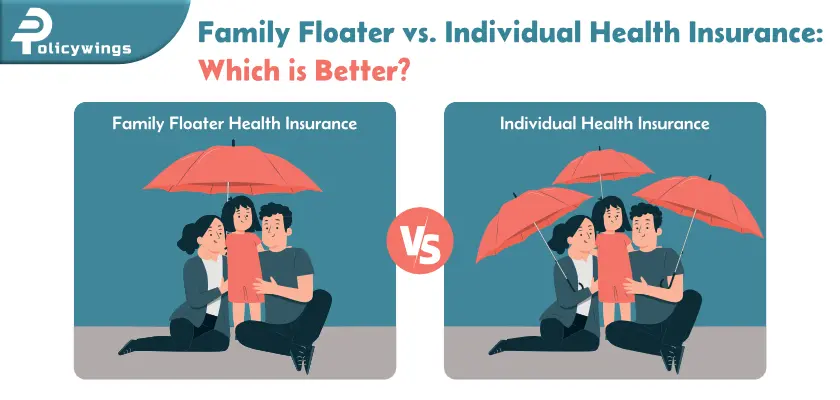

Family Floater vs. Individual Health Insurance: Which is Better?

Family Floater vs. Individual Health Insurance: Which is Better?

Table of Contents

- Family Floater vs. Individual Health Insurance: Which is Better?

- Individual Health Insurance Plan

- Family Floater Health Insurance

- How Individual Health Insurance Plans Work?

- How Family Floater Health Insurance Works?

- Family Floater vs. Individual Health Insurance

- Which is Better Among Both?

- To Sum Up,

- Some Frequently Asked Questions

Family Floater vs. Individual Health Insurance: Which is Better?

We discussed the importance of family floater health insurance in our last article. Afterward, we realized we had to differentiate between family floater health insurance and individual health insurance. People are aware of the importance of having health insurance, but when it comes to making a decision, they are unable to choose between individual and family floater plans. That’s why, to help you choose between the two, we will discuss, family floater vs. individual health insurance so that you can easily pick one among them. But to differentiate between both, first, let’s understand what are individual health insurance policies and family floater health insurance policies.

Individual Health Insurance Plan

It’s already clear by the name, individual health insurance gives health coverage to a single individual. That also means, it won’t cover your family members in one plan, instead, it will provide a separate individual plan to cover the health benefits of that individual. An individual health insurance plan is best if you have an elderly parent with serious health issues or if you want to protect your individual health needs.

Family Floater Health Insurance

Contrary to individual health insurance plans, a family floater health insurance is a plan that protects you and your family members under one single plan. So, the total sum insured is shared amongst all family members. A family floater health insurance is a smarter option to protect the entire family’s health and finances under the name of one insurance.

How Individual Health Insurance Plans Work?

The individual health plan is brought in the name of an individual, and it could be the person buying itself, or the spouse, children, or parents. So here, the premium will be according to each individual’s age and the respective sum insured.

How Family Floater Health Insurance Works?

In the case of family floater health insurance, more than one member can be covered under the same plan. Such as both parents and their children can be covered together by paying only one single premium. In family floater health insurance, the entire sum insured can be availed by any of the listed family members and is not restricted to only one individual.

Family Floater vs. Individual Health Insurance

To better understand which health insurance policy can serve you better, here is the differentiating table for both individual and family floater health insurance policies.

Features

Individual Health Insurance

Family Floater Health Insurance

Premium

Premium is based on the age and health condition of the individual. If calculated, Individual health insurance premiums are higher than family floater premiums.

Premium is based on the age and health condition of the eldest member of the family You have to pay a single premium amount for a number of members.

Coverage

Covers medical expenses of the insured individual

Covers medical expenses of all family members under a single sum insured.

Sum Insured

Generally less than the amount insured under family floater plans.

Higher sum insured shared among all family members.

Claim Settlement

Individual claims do not affect other members.

Claims made by one family member affect the overall sum insured.

Which is Better Among Both?

So to be very clear, your health insurance premium will be low if you choose a family floater policy, because both the premium and sum insured will be shared among all the family members. So, if you have a family with no major chronic disease history or have little kids, buying a family floater plan is a good option. But, if you have a family history of some chronic issue or one member in the family suffers from chronic health issues then in that case, buying an individual health insurance plan will be suitable.

To Sum Up,

The preference for buying a health insurance policy entirely depends on the individual and their dependents. Both plans have their own pros and cons. Furthermore, when comparing family floater health insurance and individual health policies, the budget is the primary differentiator. When choosing which policy to purchase, be sure to compare the budgets of the two. Nevertheless, having health insurance always has long-term advantages and gives you security, even in times of emergency, regardless of the kind of policy you purchase. That is why, setting aside a small amount of money each month for a family floater or individual health insurance will prevent you from having unplanned, high costs. Additionally, if you are still unsure, contact us, and our team will assist you in obtaining the best health insurance plan in the area.

Some Frequently Asked Questions

Is family insurance better than individual?

The answer to this question depends entirely on your needs and priorities. Family insurance can be cost-effective and provide comprehensive coverage for multiple family members in a single policy, which is beneficial for families. Individual insurance, on the other hand, offers tailored coverage for specific needs, which can be beneficial for individuals without dependents.

What are the disadvantages of the family floater mediclaim policy?

The only disadvantage of a family floater mediclaim policy is the limited coverage for each family member.

Can I change the family floater to the individual?

Changing a family floater health insurance plan to an individual health insurance plan is not that straightforward. It involves, canceling the existing family floater plan and buying a new individual health insurance plan. However, this can lead to a potential loss of benefits.

Who Cannot be covered under a family floater policy?

A family floater policy might not cover certain people, such as grandparents, siblings, and other extended family members who do not reside with the insured family, people who have pre-existing medical conditions, and people who are older than the upper age limit set by the insurance company.

What is the age limit for family floaters?

Family floater policies typically cover people from birth to old age, though some may go up to age 65 or 70 for adults. The exact age limit varies depending on the insurance company.

{"@context":"https:\/\/schema.org","@type":"FAQPage","mainEntity":[{"@type":"Question","name":"Is family insurance better than individual?","acceptedAnswer":{"@type":"Answer","text":"

The answer to this question depends entirely on your needs and priorities. Family insurance can be cost-effective and provide comprehensive coverage for multiple family members in a single policy, which is beneficial for families. Individual insurance, on the other hand, offers tailored coverage for specific needs, which can be beneficial for individuals without dependents.<\/p>"}},{"@type":"Question","name":"What are the disadvantages of the family floater mediclaim policy?","acceptedAnswer":{"@type":"Answer","text":"

The only disadvantage of a family floater mediclaim policy is the limited coverage for each family member. <\/p>"}},{"@type":"Question","name":"Can I change the family floater to the individual?","acceptedAnswer":{"@type":"Answer","text":"

Changing a family floater health insurance plan to an individual health insurance plan is not that straightforward. It involves, canceling the existing family floater plan and buying a new individual health insurance plan. However, this can lead to a potential loss of benefits. <\/p>"}},{"@type":"Question","name":"Who Cannot be covered under a family floater policy?","acceptedAnswer":{"@type":"Answer","text":"

A family floater policy might not cover certain people, such as grandparents, siblings, and other extended family members who do not reside with the insured family, people who have pre-existing medical conditions, and people who are older than the upper age limit set by the insurance company.<\/p>"}},{"@type":"Question","name":"What is the age limit for family floaters?","acceptedAnswer":{"@type":"Answer","text":"

Family floater policies typically cover people from birth to old age, though some may go up to age 65 or 70 for adults. The exact age limit varies depending on the insurance company.<\/p>"}}]}